Last updated on October 23rd, 2024 at 02:30 pm

So let’s start with an example straight forward which will make the beyond budgeting CIMA concept very clear. Let’s say you created a company-level budget stating that you will spend $20,000 in marketing, $1000 in transportation of the products, and $30000 in salary. However, when the actual implementation was in hand, you found that the shipping costs could be reduced to zero by charging the customer the delivery charges itself.

Now, in this sense, a traditional budgeting method would force you to spend that $1000 even if now its useless. But why? Well, so that in the coming year you get allotted $1000 for transportation. This is where the most likely purpose of budgeting falls right on its belly.

Characteristics of Beyond Budgeting CIMA

Now let me discuss some key features of beyond budgeting which will simplify things for you.

- Beyond budgeting CIMA is not constant but adaptive. So instead of an annual budget it would be a rolling budget. For example, based on a quarter or monthly frequency.

- Secondly, the same budget you will also create making sure that you are linking it with the key performance indicators. For example; Let’s say you are planning that one of our key performance indicators is that the revenue should grow by 20%. So then what are the budgetary allocation that you will do to make sure that the budget is allocated to make sure that growth happens.

- Thirdly budgeting allocation also depends on benchmarking your team’s performance not just internally but externally to the industry.

- Also, focus has to be on making sure that budgets should be targeted to improve the future performance and not be derived just basis what has happened in the past.

Traditional Budgeting Vs Beyond Budgeting CIMA

| Traditional Budgeting | Beyond Budgeting CIMA | |

| Targets & Rewards | Incremental targets, fixed incentives | Stretch goals and targets with incentive |

| Planning and controls | Fixed annual plans | Continuous planning |

| Resource and coordination | Pre allocated resources | Dynamic resource allocation |

| Organisational culture | Central control | Local control |

Beyond budgeting is:

‘An idea that companies need to move beyond budgeting because of the inherent flaws in budgeting especially when used to set contracts. It is argued that a range of techniques, such as rolling forecasts and market-related targets, can take the place of traditional budgeting.’

CIMA Official Terminology, 2005

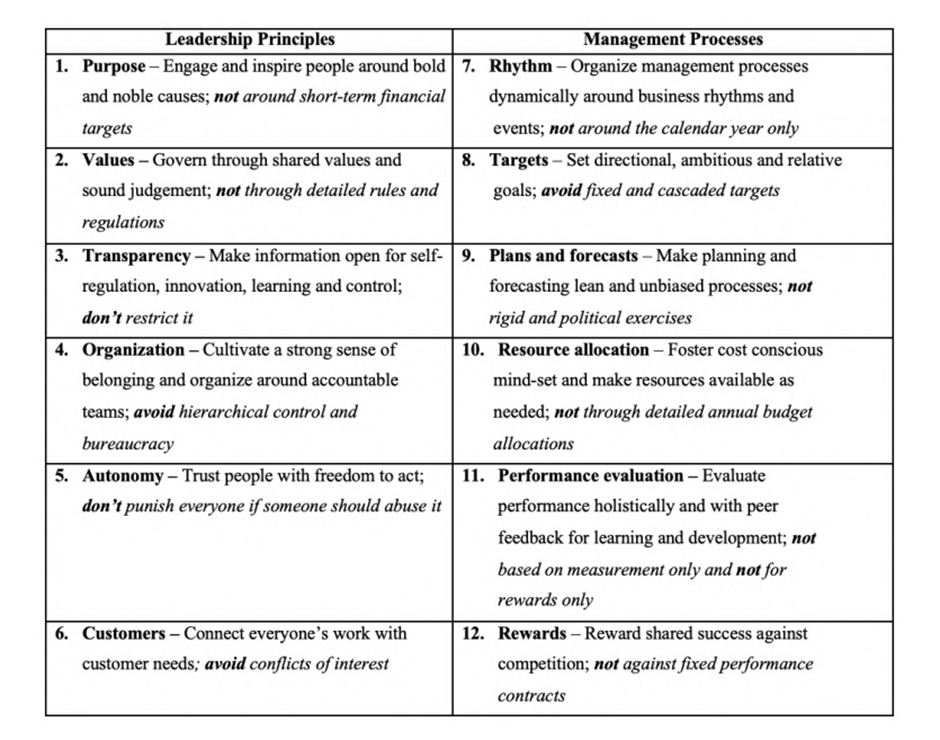

Beyond Budgeting CIMA Principles

Challenges

Now as much as it looks attractive and doable beyond budgeting has not really got implemented with all possible organisations. So let me take you through some challenges with the beyond budgeting CIMA concept.

- Firstly the 12 principles of beyond budgeting are too generic and not specific

- Concepts like business agility or agile management are somewhat similar to the beyond budgeting concept

- Secondly concepts like okr or objectives and key results are somewhat similar to the beyond budgeting concepts.

- Beyond budgeting almost proposes that there should be no budget however companies without budget can be on the other extreme.

Case Study Beyond Budgeting

The case company here is Agro Foods company with annual turnover of $5 billion and with more than 15000 employees. The company is structured as a cooperative and is owned by farmers of India. The members are not only the owners but also the suppliers of the food company. As part of restructuring its business’s the company started closely examining its processes to implement the beyond budgeting concepts.

What changes were implemented?

Annual Target:

So first and foremost the company set out a peer group benchmark. Followed by setting an annual target which was subdivided to divisions and division level budgets were set.

Higher Level of Detailing

What this did was that since the target was subdivided across smaller units and hence smaller levels of details were added in the budget to make sure that the target was achieved.

Discussions & Conclusions

In summary it can be said that the beyond budgeting concept is definitely unique and innovative. However the same comes with challenges like setting a peer benchmarking which is one of the most challenging aspects of beyond budgeting. However another challenge with any budget is with level of uncertainty. Higher level of uncertainty means that a budget is expected to change more than less.